The 401k has essentially replaced pensions as the dominant way that people save for retirement. Regardless of whether you think that is good or bad it generally creates much more choices for employee investors. Few companies can or will give advice on fund selection and the companies who provide the system to the company may not have their interests aligned with employees.

So I tried to put together a fairly simple way to help pick.

WHAT TO AVOID

1) Avoid Return Chasing.

Probably one of the worst things you can do is filter by 3, 5 and 10 year returns and pick the one that has the highest return. It’s been proven over and over again that “past performance is no guarantee of future results. Actually in many cases the reverse is true. The better the past returns, the more people tend to pile in and thus the price of the investment has gone up a lot meaning that a normal “regression to the mean” will cause future performance to be worse.

Don’t get clever and try to buy the worst performing funds either because many funds disappear completely leaving the investor with $0.

2) Avoid Making things complex.

I think it’s wise to stick to 2-4 funds. Anything more gets really messy and complicated. You have to start thinking about which companies the funds hold and in what %, because there might be lots of investment overlap. You have to understand the different strategies used by the different fund managers. You have pay more attention to which indexes they compare themselves against. Additionally this generally has very little effect on long term overall performance of the investment, and it leads to “activity” by the investor that is almost always negative for returns.

3) Avoid looking at it too much.

In many situations monitoring and information are powerful tools. In investing they can be just as effective as blowing you up and giving you increased performance. Money has a huge impact on our emotions and losing it is really scary (I’m sure many of you are feeling that after “Brexit” last week). Those big moves up and down make us react in ways that are generally bad for our long term investment performance. The best advice I can have is to try to not look at your portfolio very often. Maybe a couple times a year or once a month at most; and decide in advance what you are going to do (or not do) and when you are going to do it.

WHAT TO DO

Let’s pretend we have 100k in our 401k with Fidelity, where should we put it?

1) Max any Matching

401k matching is free money. Of course ever article ever written about 401Ks says to do this. For some people it’s really hard because they are living on every dollar they earn. Still… if you can, cut things out of your budget… maybe that coffee in the morning or go out to eat less or whatever. If your employer has a match not only do you get double dollars, you also get them Tax free AND you get to avoid taxes on the compounding earnings over many decades (assuming you are younger).

A strategy I used when I was younger was upping it by 1% every 6 months to a year. A 1% pretax drop in my pay isn’t that noticeable, but over 3-4 years it increases contributions to 5%+ and that can have a HUGE impact over 30 years. It’s the boiling frog, but in this case it makes you richer instead of killing you :).

2) Define your risk tolerance and asset allocation.

This can be really tricky for people. Traditionally it comes down to stocks, bonds and cash. Since cash is elsewhere, the 401k really comes down to stocks and bonds. My suggesting is if you don’t know what your risk tolerance is and you are going crazy thinking about whether the market is high or low or if you should subtract your age from 120 and then set your % or if you’re a little older now, or if the bond market is overpriced. I’d keep it simple and just take 70/30 stocks/bonds and start from there.

3) Focus on fees.

When I look at which investments to make I use fees as the #1 filter. Here’s why.

Assume you have 100k in your 401k and assume that on average it will return 4% inflation adjusted a year for the next 30 years.

That initial 100k represents a “job” that “pays” you $4,000/year.

I think of fees as a “tax” on my INCOME as opposed to a cost on the PRINCIPAL. So when I evaluate fee impact I don’t do this:

100,000 * (1% fee) = 1000/year. “Wow. That’s only 1% of my money, that doesn’t seem like much.”

I do this

$4,000 income from job / $1,000 fee = 25%. “Hang on. The fund is taking 25% of my money? That seems really high.”

I’m convinced that second way is the way to evaluate ANY investment service that take a % of your money.

LET’S MAKE OUR CHOICES

So we have 70k to put in stocks and 30k to put in bonds, which ones?

STOCK SELECTION

So my first goal is to find the funds with the lowest fees.

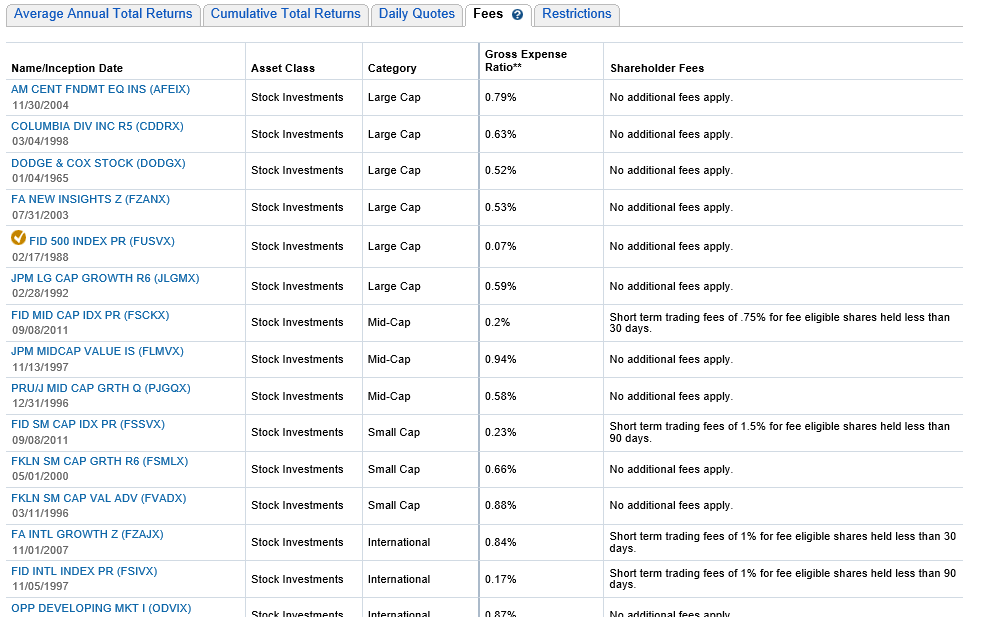

Fidelity lets me do this pretty easily as I can browse the investment choices and show the fees in a nice list (they don’t let me sort by fees, so it’s a bit more work). Here’s what it looks like:

You can see that the first tab is annual returns, followed by cumulative total returns. That’s what most people use. I barely look at them because I consider them mostly noise.

I’m VERY interested in that gross expense ratio. The lowest one is the FID 500 Index PR at 0.07%. The highest one is the JPM Midcap Value IS at 0.94%. Now all of these fees are pretty decent as many go up to and above 2%; which in our 4% long term return world is 50% of our income. No way.

I honestly think 1.5%+ fees in 401Ks should be pretty much banned. In fact I think anything over 0.5% has no business being in a 401k because it’s just acting as a wealth transfer mechanism from the middle class to the wealthy institutional investors by capitalizing on people’s ignorance. 401k managers who recommend funds that charge 1%+ without major disclosures and resistence (either in person or via automation) should be ashamed of themselves. But that’s just my opinion.

Personally I omit all funds and ETFs that charge more than 0.5%. More generally, unless there is a really strong reason to the contrary, I won’t give anyone more than 0.5% of my investment, period.

In my situation it limits me to a handful of choices. There’s a midcap index, a smallcap index, an international fund, etc. What I would normally look for is some kind of global fund (Vanguard has one called VT that is basically the world stock market in one fund). The other way to do it is to split it into “domestic” (for me the US) and International.

The best domestic option I have is the FID 500 INDEX PR (FUSVX) which basically tries to duplicate the behavior of the S&P 500.

Most people know that VERY few professional investors beat the S&P 500 over time so that combined with the small fees makes it by far the best choice open to me.

For international the best choice is FID INTL INDEX PR (FSIVX) fund because it has a low fee of 0.17% and good diversification. It’s also NON-US which means there will be very little overlap with the FUSVX.

Personally I would put ALL of the 70% into the FUSVX because it’s by far the lowest fees for the diversification. Many people argue that the S&P isn’t well diversified because it’s all big US companies. That’s partially true, but many of those companies get much of their revenue from global sources so it’s far more diverse than it looks. It DOES focus on large companies, but I think the smaller the company and the more focused the investment the more you have to know to invest and this is about SIMPLE choices.

It would be totally reasonable for me to put half of the 75% in FUSVX and half into FSIVX. I just really hate fees and think the S&P 500 is pretty well diversified globally, so that’s what I would do and what I would recommend.

BOND SELECTION

Bond selection is not different. Fidelity doesn’t let me easily filter so I have to find the bond funds inside of that list.

The lowest fee is the FID US BOND IDX PR (FSITX) at 0.17%. Similarly there’s high yield bond funds, international bond funds, and so on, but since bond investments tend to be the more stable/less return part of the portfolio fees matter even more. FSITX is invested in US government and corporate bonds in a pretty “normal” way.

So I would put the full 30% there.

That means I’m omitting international bond exposure which can be argued is not diversified enough. Unfortunately, the best choice for me was the AB GLOBAL BOND Z, but it’s fees are way higher (0.53%) and it’s 40% US Bonds anyway.

A NOTE ON TARGET DATE FUNDS

Fidelity (and most major 401k providers) have so-called “Target Date” funds which seek to adjust the risk structure based on a targeted date (usually for retirement).

So let’s say you pick FITWX which has a target date of 2025. As it gets closer to 2025 the fund will move more of it’s assets into “less risky” assets such as bonds and cash. It’s basically a well diversified, age adjusted and rebalanced portfolio all in one.

I think these are great, but I HATE the 0.55%-0.77% fees. Vanguard, for example, has a 2025 target date fund that has 0.15% expense ratio. I’m not going to pay 3.5 times more than I could for the privilege of having the word Fidelity on the fund. Sorry.

If the fidelity fund had a competitive fee, I’d just put everything in that and move on. I just can’t pay that 0.66% fee when there’s far cheaper and nearly as simple alternatives. So if your provider has a target date fund that has reasonable fees, I’d probably go with that; and if I roll my 401k over; I’d probably put it into a Vanguard target date fund that matches my expected retirement date.

SUMMARY

So there you have it. 2 investments, simple choices, fairly broad diversification, low stress.

Of course WHAT the market returns I can neither control or predict.

I can control fees so I monitor them and adjust as needed (hasn’t been needed in last 4 years).

I can control spending (to some extent) and thus I can max the matching.

I can control taxes (to some extent) and thus reduce my income liability by saving more in my 401k.

Hope this is helpful!

I've been thinking a lot about this recently, and it always makes me wonder one thing: what assumptions about the future would make you decide that investing in the S&P 500 (or similar index) is a *bad* idea? (Assume that I tend to value safety over performance for my 401k in the long run)

It's a good question.

To me it's not about a good or bad idea, it's about better or worse than comparable options.

Historically going back 80+ years the S&P beats almost everything over a multi decade time horizon. That includes a great depression, world wars, nuclear threat, leaving the gold standard and so on.

But let's assume the future is worse. OK. So what is safe? Individual stocks? Well… if you can pick well sure.

Gold? Most people own gold in the form of slips of paper. In a major revolution those pieces of paper will be just as valuable as the stock.

You could hold physical gold but it has risk of theft and high transaction costs. Also… it's not a producing asset so you have to hope someone is willing to pay more. And then in a major collapse you have to protect it long enough to spend it :).

Cash gets crushed by inflation so evil though it has low volatility, it is almost guaranteed to shrink in value around 3% per year.

Safety is an illusion.

Just because we need the market to give us x… doesn't mean it will.

So… I try to focus in what I can control. Taxes, fees and my own spending.

If I keep spending low, taxes optimized and fees reasonable I'll probably be better at keeping whatever the market returns are than if I don't.

What those returns are I don't know and I haven't figured out a way to control or predict them :).

Something I have considered though is when the S&P becomes less good than in the past. As an exaggerated example imagine the top 500 earners right now earn 50% of America's GDP, but that 50 years from now a bunch of smaller companies become the norm instead of megacorps and now it only earns 0.1% of it. Maybe another index would have been safer in that case.

I know we can't do much with that information other than diversify a bit in a different direction, but it doesn't feel safe to me to just ignore the possibility. Assumptions of "investing in X is safe because it has always been safe" are where things like the '08 crash come from.

And what if it continues the way it has in the past :). You tell me what will happen and I'll tell you how to invest :). Things can be completely different in the future than they were in the past and the long term trend data can be completely upended… but I don't know a more reliable way.

A well diversified stock/bond portfolio held since 2000 has done OK despite 2 manor recessions.

If you put all your money into the S&P just before the 1929 crash you would have beaten nearly any other investment… gold, cash, real estate, etc.

It's not perfect but I think broadly diversified portfolios is the least risky thing there is… risk being uncertainty of the future.