Healthcare is a very hot topic these days. Regardless of how you feel about the topic, I feel it’s important to understand which are the critical statistics and how they can be visualized.

There are things about healthcare that make it very different than other markets such as food or cars or houses.

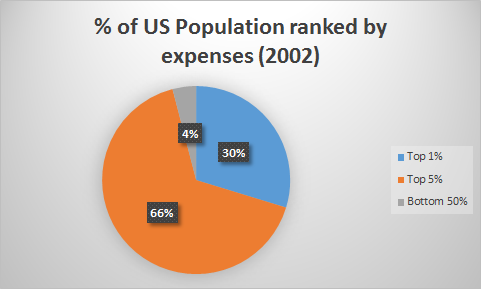

COST DISTRIBUTION

I think the most remarkable and critical element of the healthcare “market” is that the costs are INCREDIBLY concentrated.

Essentially 1% of people generate 30% of all medical costs and the bottom half of the population is responsible for only 4% of health spending.

While this is from 2002, the data is fairly consistent going back many decades. It’s also hardly surprising. From our own experience we can probably recall incidents of ourselves or others having extreme situations that become very expensive with large time periods and most people never having any major problems.

Because of this any healthcare market must draw from a large number of healthy people to pay for a small number of very sick people at any given time. Bear in mind that 1% of people costing 30% is a unit in time. As you can imagine, when you get older your chances of entering that 1% become much greater. So possibly a 401k type health cost insurance system might make sense. That is, you may MORE when you are younger and “save up” for disaster in the future.

Of course we could also let the top 1% and 5% die, reducing the costs massively, but this is not the kind of society we choose to live in.

So, we must design a market system that is built for the EDGE cases and not the MEDIAN cases because it’s the edge cases that are responsible for the large costs.

COMPLEXITY OF MARKET

When you buy a car there are things like truecar, cars.com, Car and Driver and so on to provide consumers with objective and comparable information when making a decision. There is no such tool for the healthcare market. Indeed, medical costs at hospitals are incredibly difficult to decipher.

First, things like “Asprin” can be called by many different names.

Brand names: Ecotrin, Bayer Aspirin, Acetylsalicylic Acid, Aspir 81

Second, the charges are separated from the underlying costs.

That is, on the hospital bill will appear “Ecotrin: 25$.” How can the average consumer possibly know they just spent 25$ on asprin? If you itemize 10 or 100 such things, it’s not reasonable to assume that any patient can possibly be educated enough to negotiate their bill.

LACK OF EMPOWERED DECISION MAKING AND BARGAINING POWER

The customer has no options at the point of use.

Both before and during hospitalization, you have very little time to make any kind of consumer based decision. If you’re in a car accident and unconscious, how can you possibly make sure the ambulance takes you to an “in network” hospital? When you are undergoing surgery, how can you possibly insure that your doctor takes your insurance, or what her rates are? Or if other hospitals and other doctors might offer the same services for less cost?

Also, let’s say you’re lying in bed and you are given a 25$ aspirin. Are you really in the position to ask how much the pill costs and then pop down to Walgreen’s and buy it yourself? Not really.

So when people suggest a more “open market” for healthcare, these factors are critical.

1% of the sickest people are unlikely to have sufficient bargaining power to influence the cost of their care. The other 99% are unlikely to be proactive and force providers to maintain reasonable prices.

Also, the providers themselves have to prepare for that 1% since that is where the costs are and if that is not somehow subsidized by the other 99%, it’s hard to imagine how they can bear those costs. Because of that their incentive is to gouge the hell out of the unlucky 1%, especially if they are uninsured as insurance companies have at least SOME amount of leverage to negotiate prices.

Medicare has one of the lowest reimbursement rates because it’s huge membership can help it exercise pricing power on health providers. A fragmented insurance marketplace doesn’t allow for that.

Part of the reason is because Medicare is not allowed to negotiate drug prices, whereas all other public health programs around the world can and do negotiate. Pharmaceutical companies resist allowing Medicare to negotiate claiming they need this in order to fund R&D, which is possibly true.

The question in my mind is why Americans are ok with subsidizing global pharmaceutical costs while not being ok with foreign imports; considering we spend much more on medication in our lifetime and can’t really do without drugs the same way we can do without TVs and smartphones. There must be SOME better way to fund R&D expenses than to have American citizens subsidize the costs of medications around the world.

SUMMARY

The nature of the healthcare market require us to design a system that is focused on outliers… not the average. It must also distribute those concentrated costs broadly. Finally, it must be regulated in some way to address the information gap and bargaining power gap between providers and users generated by the nature of the system (that is, when you need care is exactly when you are in the worst position to negotiate).

{kind=link}